Laws, Regulations and Industry

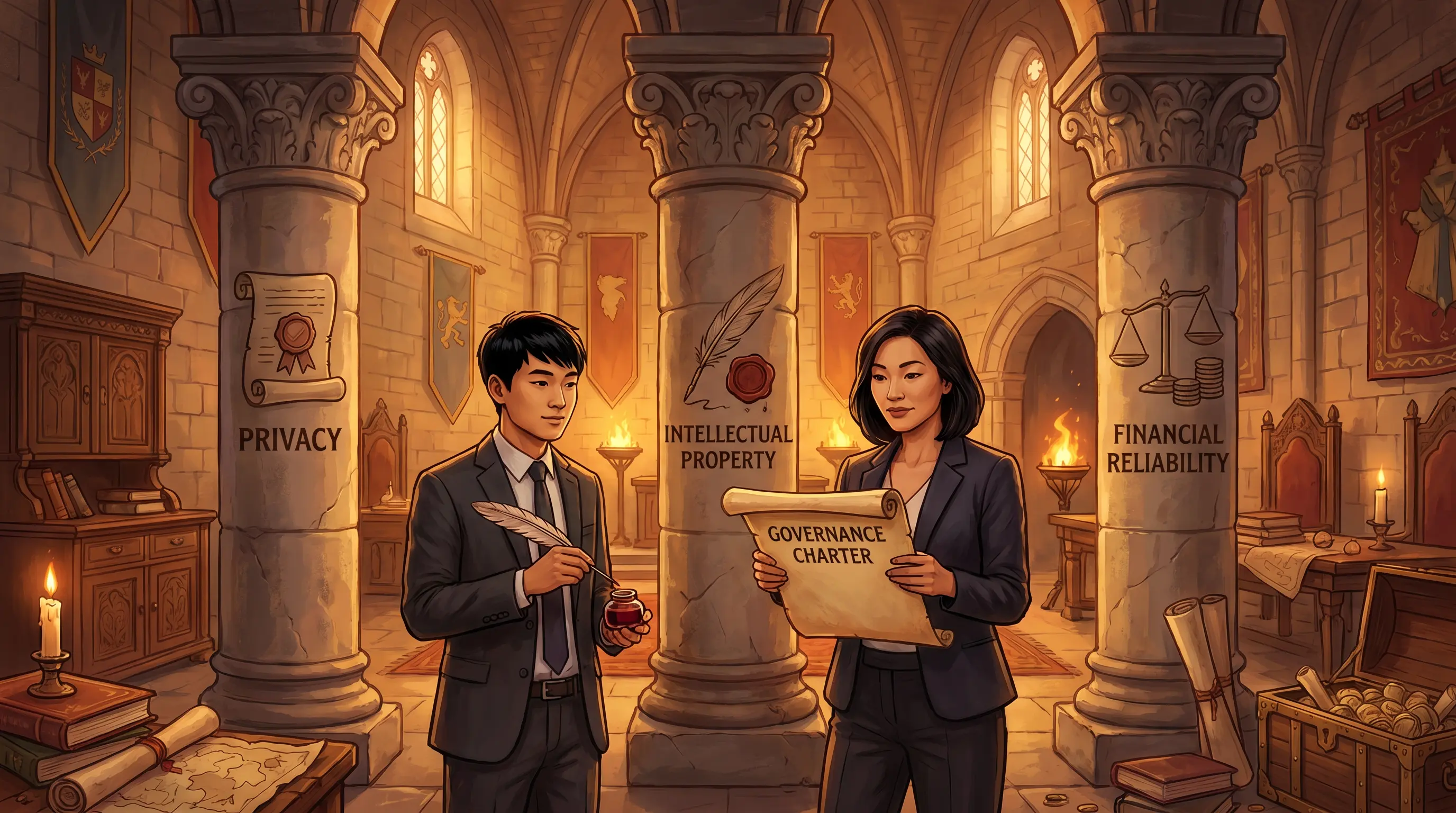

Sarah Lin drops a printed regulatory summary on Alex Chen's desk before the quarterly governance review. Meridian has just expanded its mortgage-data service to EU retail clients, and three lines are highlighted in yellow: GDPR now applies. Alex scans the IT governance charter — last updated four years ago — and finds no mention of data-subject rights, cross-border transfer controls, or a designated privacy officer role. The charter was current when written. It is not current now. The compliance review meeting starts in ten minutes. Should Alex raise the charter gap as a finding, request a scope extension, or simply note it as a background observation?

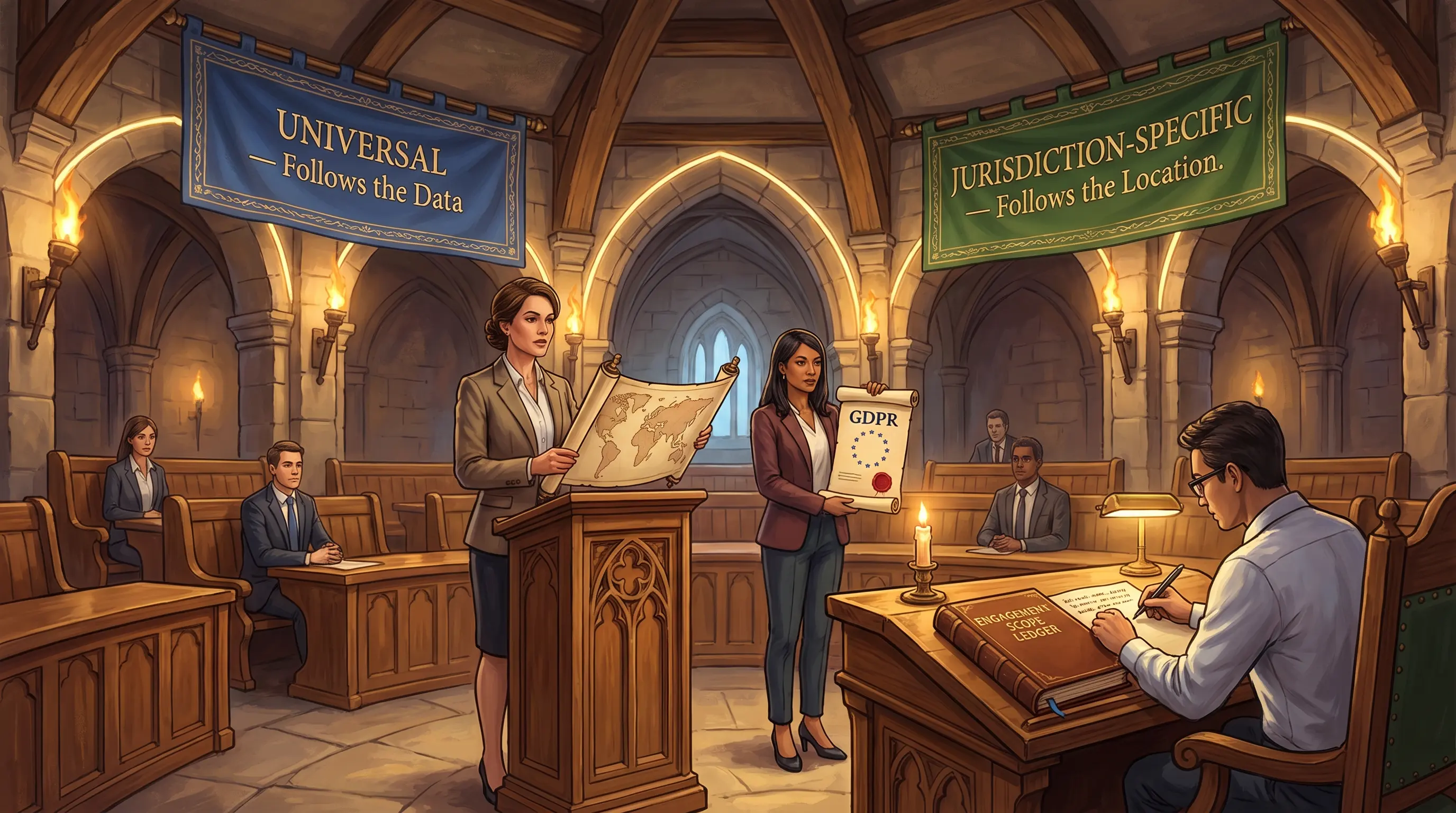

IT governance must account for the legal and regulatory environment in which an enterprise operates. Laws and regulations differ by country and industry, but three compliance categories are recognized globally: the protection of privacy and confidentiality of personal data, intellectual property rights, and the reliability of financial reporting. Because these requirements evolve continuously, the IS auditor must ensure the enterprise's governance framework is reviewed and updated regularly. Enterprises operating across multiple jurisdictions face layered obligations — a regulation enacted in one region may impose requirements on any organization that handles data related to individuals in that region, regardless of where the enterprise is headquartered. The IS auditor's role is to identify which rules apply, verify the enterprise is meeting them, and flag gaps when the governance framework has fallen out of date.

Privacy & Confidentiality

How is personal data protected across its lifecycle?

- Receipt and collection controls

- Processing and storage requirements

- Transmission restrictions

- Destruction standards

Intellectual Property

Are software and data assets properly licensed?

- Software licensing compliance

- Open-source usage controls

- Data usage rights

- Creative asset authorization

Financial Reliability

Is financial information produced accurately and auditably?

- Accurate financial reporting

- Auditable IT controls (SOX)

- Integrity of financial systems

- Management sign-off requirements

Auditor's Obligation

What must the IS auditor do continuously?

- Track evolving regulations

- Identify applicable rules by jurisdiction

- Flag outdated governance frameworks

- Document consciously accepted noncompliance risk

Meridian Corp operates in the US banking sector and processes customer data for EU clients. The IS auditor is scoping the compliance review. The team debates whether GDPR applies because Meridian is US-headquartered. What is the legal basis for including EU regulatory requirements in the scope, regardless of Meridian's headquarters location?

IT governance must account for laws and regulations that vary by geography and industry but converge on three globally recognized compliance pillars:

- Privacy and confidentiality of personal data — protecting how data is received, processed, stored, transmitted, and destroyed

- Intellectual property rights — ensuring software, data, and creative assets are used with proper authorization

- Reliability of financial information — satisfying requirements around accurate, auditable reporting

Beyond these universal pillars, industry-specific rules (such as regulations on electronic communication in brokerage firms) add further obligations. The IS auditor must track which rules apply to the enterprise's specific geography and industry and flag when compliance posture is outdated.

The CISA exam does NOT test knowledge of specific statutes. It tests whether you recognize (a) the three globally recognized compliance pillars, (b) that regulations can apply to enterprises outside the jurisdiction of enactment, and (c) that an enterprise may consciously choose to accept noncompliance risk — but that decision must be documented and approved.