IS Audit Standards, Guidelines, Functions and Codes of Ethics

Alex Chen's first week at Meridian Corp ends with a pointed question from Priya Rao: 'The board is asking what gives our audit conclusions any weight. I want you to brief them tomorrow morning — three elements, what each one does, why we can't replace any of them with just good judgment.' Alex stares at the empty slide deck. He knows the framework exists; he's never had to defend why it exists. Priya adds: 'A board member is going to ask whether Guidelines are optional. You need to know what to say before they ask it.'

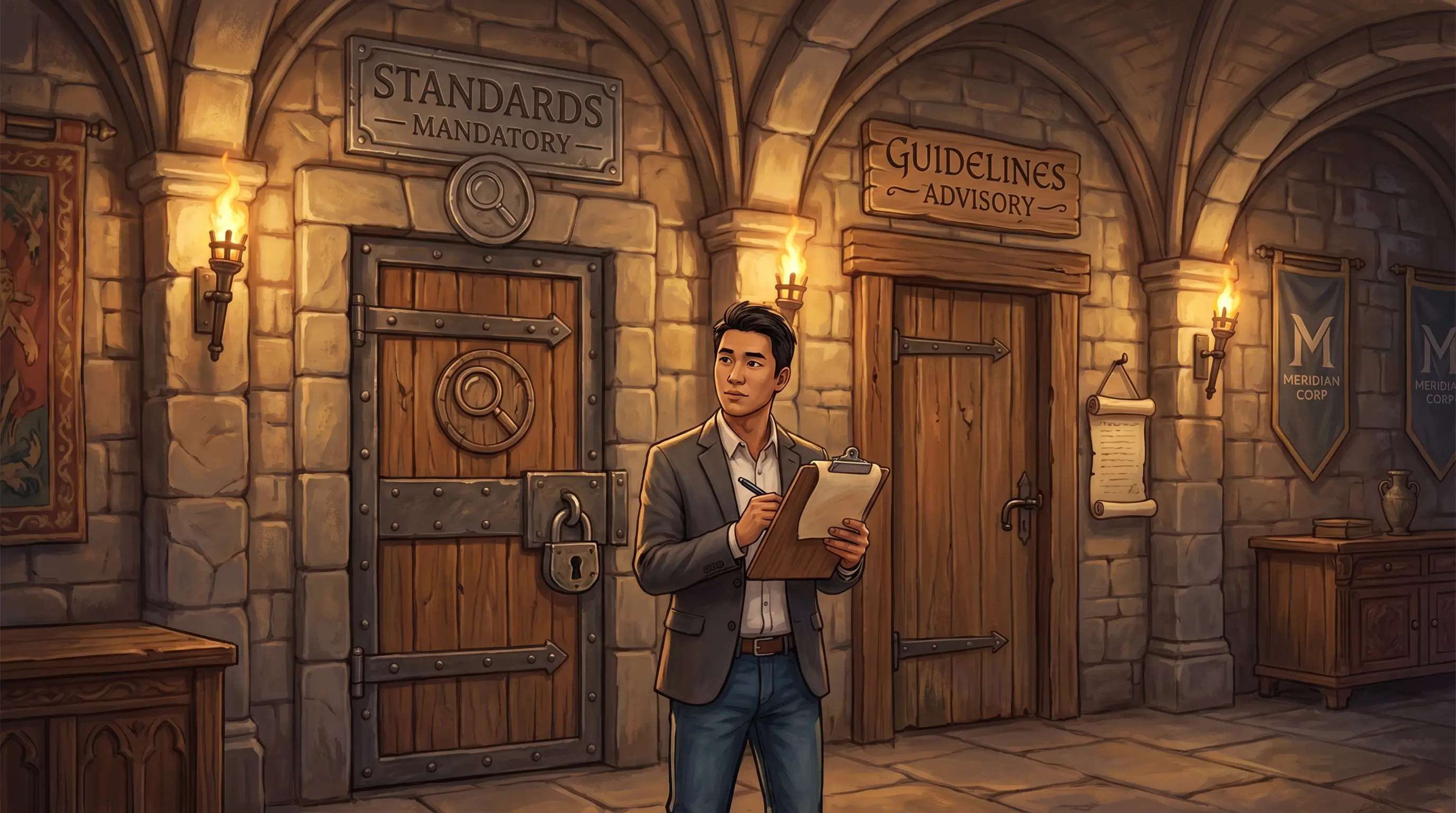

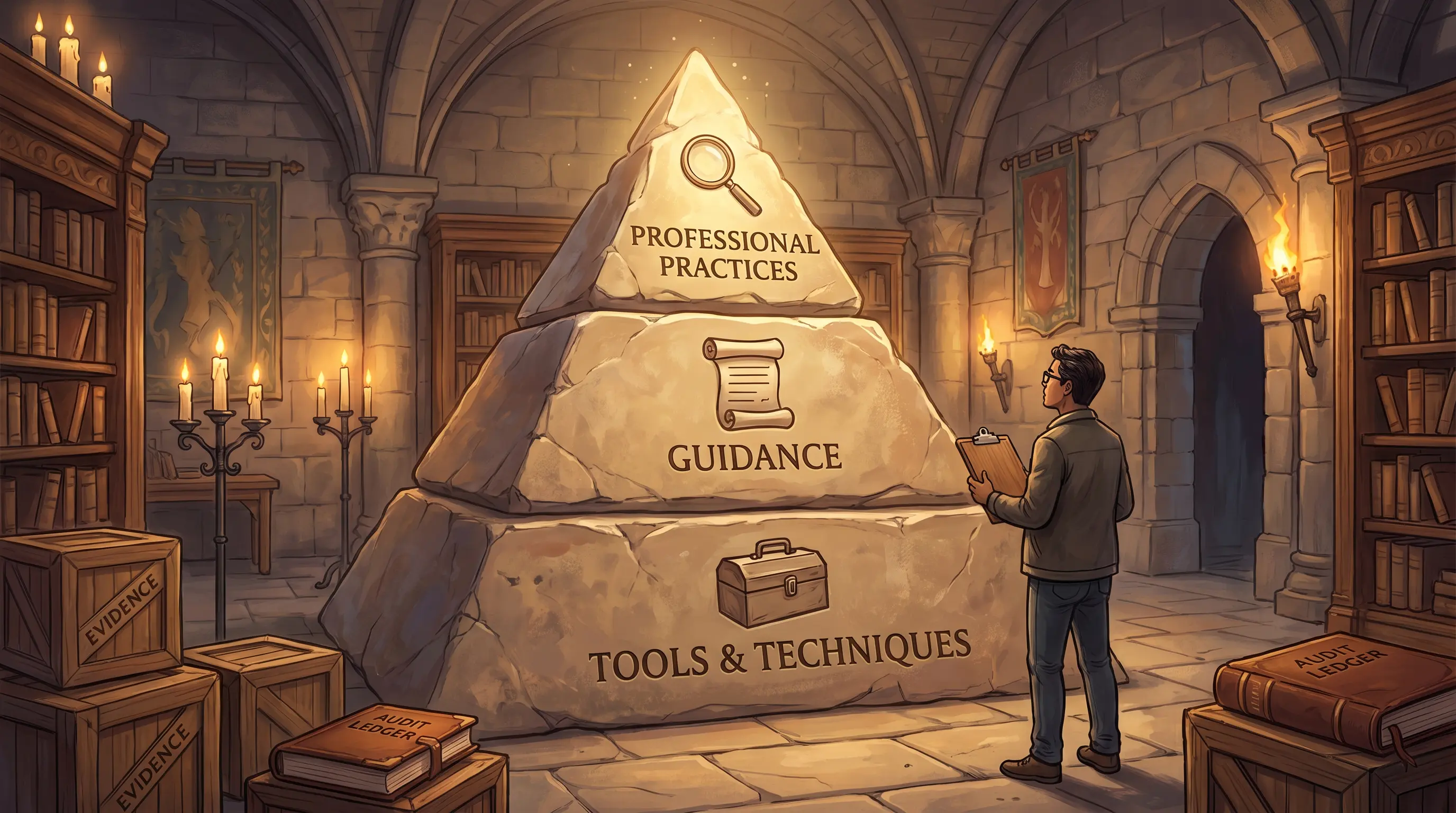

IS audit credibility rests on three foundational elements defined by ISACA. Standards state the mandatory requirements that every IS auditor must satisfy — they define the minimum acceptable performance for IS auditing and reporting. Guidelines provide supporting guidance on how to comply with those standards, leaving room for professional judgment in specific circumstances. The Code of Professional Ethics governs the professional and personal conduct of ISACA members and certification holders. While standards are mandatory, guidelines are advisory — auditors should consider them and use professional judgment to determine the appropriate application. Together, these three elements ensure that IS audit conclusions carry authority with management, boards, and regulators.

Standards

What makes IS audit requirements mandatory?

- Define minimum acceptable performance

- Mandatory for all IS auditors

- Cover auditing and reporting

- Set by ISACA

Guidelines

How does an auditor know how to apply standards?

- Advisory, not mandatory

- Explain how to comply with standards

- Allow professional judgment

- Provide context-specific application

Code of Ethics

What governs auditor conduct beyond technical rules?

- Applies to all ISACA members

- Covers professional AND personal conduct

- Binding on CISA holders

- Foundation of audit credibility

A new IS auditor at Meridian Corp asks: 'Why do we follow ISACA's framework at all — can't we just use professional judgment?' What is the key distinction between Standards and Guidelines that explains why professional judgment alone is insufficient?

Three interlocking elements give IS audit its credibility. Standards define mandatory requirements — the minimum acceptable performance any IS auditor must meet. Guidelines explain how to implement those standards, using professional judgment to adapt to context. The Code of Professional Ethics governs the professional and personal conduct of ISACA members and CISA holders, establishing the integrity foundation on which the whole framework rests. Without adherence to these elements, an IS audit activity lacks the credibility stakeholders require.

The exam distinguishes mandatory (Standards) from advisory (Guidelines). If a question asks what an IS auditor 'must' do, the answer traces to Standards; what an auditor 'should consider' traces to Guidelines.